A fund manager in Singapore told me last month that he keeps a second laptop on his bedside table. He's been doing it for six years. When the US prints CPI or a major earnings call ends with a guidance cut, his phone buzzes on the nightstand and he opens the laptop and watches the after-hours tape until he can call his execution desk in New York to talk through what to do at the open.

He has adapted to this. He's good at it. But when I asked him what he'd want differently if he could redesign the system from scratch, he was quiet for a second and then said: I'd just want to be able to act when I see the news. Not eight hours later. Not after a phone call. Now.

That's the conversation that keeps coming back to me.

There's a generation of asset managers, and a generation of operators inside large fintechs and corporate treasuries, for whom holding US-listed equity exposure is the most ordinary thing in the world, except for the part where it lives behind a brokerage relationship that opens at 9:30am New York time and closes a little after four. Everything they do around that core is a workaround. After-hours sessions. Phone calls. ADRs in foreign listings. Synthetic exposure through cash-settled CFDs. Every workaround is an admission that the asset itself doesn't actually live where the demand is.

I think that's the thing tokenization fixes, and I don't think the framing the industry has been using captures it well.

What the asset is, and where it lives

The case people like to make is that tokenized stocks are cheaper, or faster, or fractionalized down to two decimal places. All true. None of those are the actual story. Discount brokers solved cheap. Robinhood solved fractional. T+1 settlement is already here for the equity leg in the US. If the only argument for a tokenized stock is that it lops a few basis points off a Schwab trade or lets you buy thirty cents of a share, the asset class doesn't get to a serious size.

The real argument is that the asset stops living inside a brokerage account and starts living inside a wallet. That sounds like a small distinction. It isn't.

When equity exposure lives in a wallet, the asset is portable. It can move into a yield strategy, into a lending pool, into a hedge against another position, into a payment, all without leaving the surface it was issued on. The Singapore fund manager doesn't need to call New York at 8pm his time to react to news. Neither does the family office in Dubai. Neither does the CFO in São Paulo who wants to allocate a slice of the company's USD treasury into tokenized US equity exposure without setting up an offshore brokerage. The action is in the same place the news is.

That's the part that scales.

Where the demand actually is

The mistake I see people making, including some good investors, is assuming tokenized stocks are a US retail product. They aren't. The US already has the most efficient retail equity market in the world. Robinhood is free, Schwab is free, fractional shares are everywhere, and the broker rails work. There's no painkiller there.

The painkiller is everywhere else.

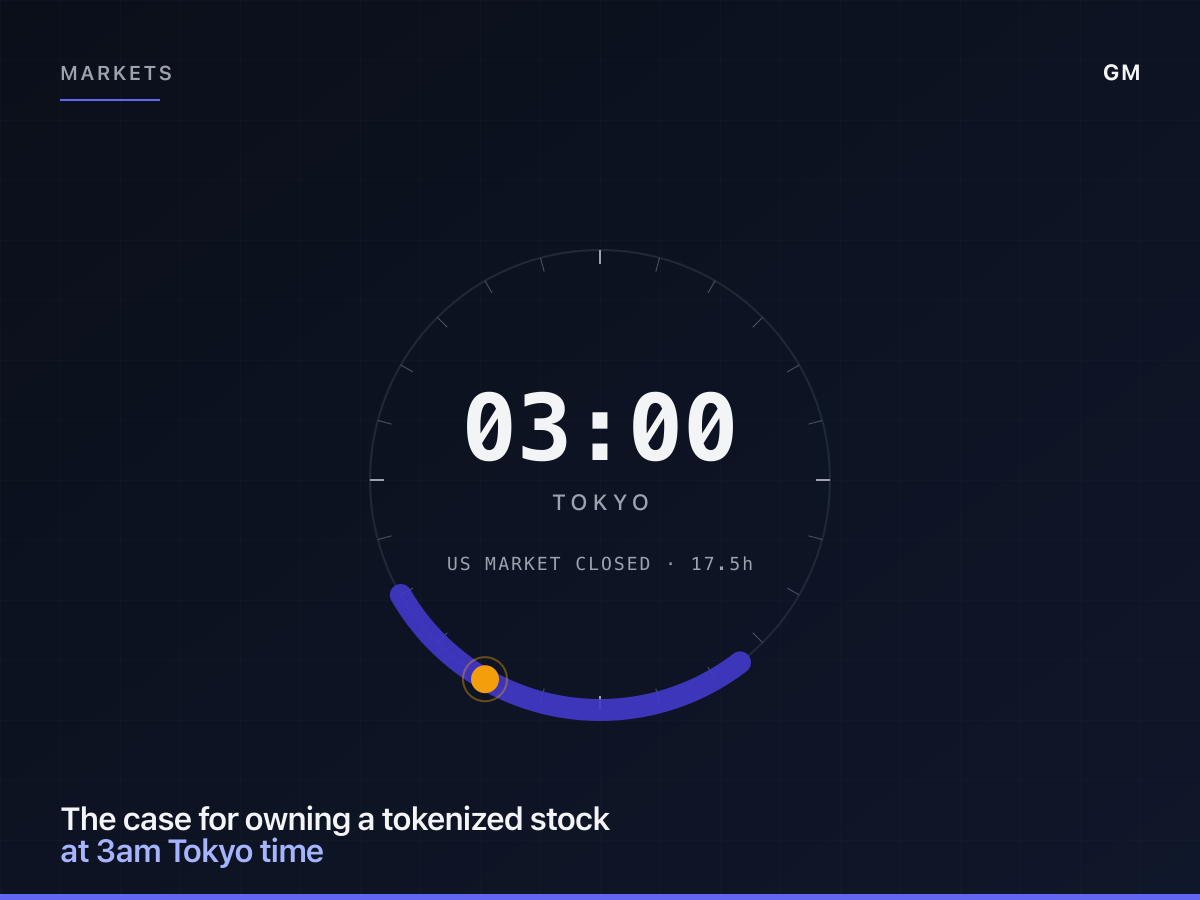

There are roughly twenty-four hours in a trading day, and the US market is open for six and a half of them. That leaves seventeen and a half hours of every weekday during which a billion-plus people in Asia and the Middle East and Africa and Latin America cannot transact in US-listed equity. Plus weekends. Plus US holidays they don't observe. The market a Tokyo-based investor lives in is structurally a part-time market.

It is not a coincidence that most of the early demand we are seeing is from outside the US. It is also not a coincidence that the demand is concentrated in places where the underlying brokerage infrastructure is the worst, and the demand for USD-denominated assets is the strongest. People are not buying tokenized stocks to save fifteen basis points. They are buying because the asset is reachable.

Why this matters more for asset managers than retail

I keep saying we are asset-manager-primary, retail-secondary, and I want to be precise about why.

A retail investor who wants global equity exposure can already get it. Slowly, expensively, with a lot of friction, but they can get it. An asset manager who runs a fund out of Singapore or Dubai or Cape Town and wants to hold US equity exposure as part of a strategy faces a different problem. The custody is split across jurisdictions. The execution windows don't line up with their portfolio cadence. The reporting comes in on three different feeds. The hedging legs settle on different cycles.

Putting the equity exposure into a wallet collapses most of that. It puts the asset in the same custody surface as the stablecoin balance, the same risk system, the same reconciliation pipeline. The portfolio becomes one set of holdings instead of three. And the manager can act when the news hits, not when the New York desk opens.

I might be drawing the lines too sharply here. There are obviously asset managers in Asia who run institutional accounts at Interactive Brokers and have figured out the workflow over a decade of practice. They are not the first wave. The first wave is the manager who is two years into building, who has not yet committed to a single broker, who looks at the workflow cost and says: why would I rebuild what stablecoins already gave us, but for the equity leg.

What 3am actually looks like

The headline is 24/7 trading, which is true and also a little reductive. The deeper story is that the rhythm of the day stops mattering.

If you run a fund in Tokyo and your portfolio includes US equity exposure, today your whole working day is shaped around the New York open. You wake up to a tape you cannot transact in. You make decisions you cannot act on for hours. You stage orders into a window that lands in the middle of dinner with your family. The shape of the day is broken because the asset lives somewhere else.

When the asset lives in a wallet, the day is yours again. The news comes in, you act on it, you move on. The phrase 24/7 misses what is actually happening, which is that the asset stops imposing a schedule on the operator.

The corollary, and this is the piece I underweighted at first, is that the underlying market is still the underlying market. There is still a real share at a real prime broker. The settlement cycle there is still T+1 for US equities and up to T+2 for some international markets. The 24/7 surface is the user's; the broker leg is not. We are absorbing the broker lag, not pretending it doesn't exist. That distinction matters when you talk to a treasurer who has been burned by a tokenization project that papered over it.

The product question this answers

Every conversation I have with a sophisticated investor eventually arrives at the same question. What does this asset class do that I cannot already do.

For a US retail investor, the answer is: not very much you can't do already. For an asset manager outside the US, or a fintech treasurer, or a family office that operates in two or three currencies, the answer is: it puts the equity leg of your portfolio inside the same surface as everything else, and it lets you act when the news happens.

That is enough to build a serious business on. I think it is more than enough. The thing I'm less sure about is how the second-order effects play out. Once the asset is wallet-native, what gets built on top of it. Lending against it. Hedging it programmatically. Paying with it. The first wave is just access. The second wave is what the asset becomes when it stops being something you have to drive to a brokerage to touch.

I might be drawing some of these lines wrong. If you're seeing the demand show up somewhere I haven't named, I'd actually like to hear about it. The shape of this is still moving, and the conversations I'm having now are not the same conversations I was having a year ago. Probably the only durable thing is that the asset is going where the user already is, and the brokerage account is the part that gets left behind.