I was on a panel at a conference last quarter, sitting next to a founder who runs a tokenization platform that has been operating since 2019. He's been at it longer than most of us. Halfway through the panel, the moderator asked us to predict where the space goes next, and the older founder gave an answer that has stuck with me. He said: tokenized is going to stop being a feature, and the platforms whose only pitch is tokenized are going to fade. The next wave is wallet-native.

He said it offhand, like he was reading the obvious. It was not obvious to most of the room. It is becoming obvious now. So I want to write down why I think he is right, and what wallet-native actually means, because the term is going to get adopted and abused in the same way "tokenized" was, and I'd like to anchor it to something more specific than vibes.

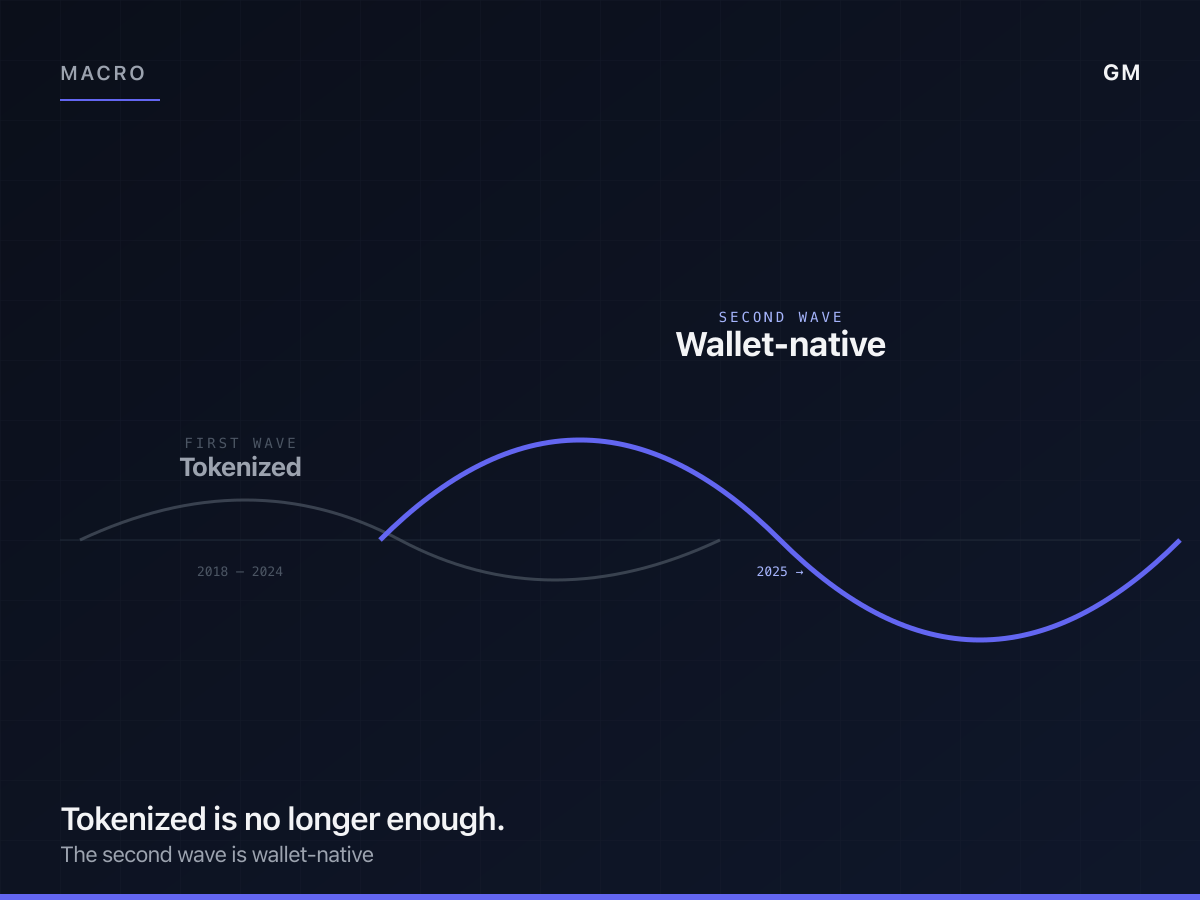

What "tokenized" meant and why it stops being enough

"Tokenized" meant, originally, that an asset existed in two places at once. The asset itself, sitting in some custody arrangement off-chain, and a token on a blockchain that represented a claim on it. The token could be traded, transferred, and accounted for on-chain. The asset stayed in its traditional plumbing.

This was a real upgrade. It made the asset auditable in a way it had not been before. It collapsed settlement on the on-chain side. It opened up new programmatic interfaces. The first wave of tokenization platforms shipped exactly this, and the platforms that did it well, like the early stablecoin issuers, captured significant value.

The thing that has happened, over the last two or three years, is that "tokenized" has stopped being a differentiator. Every serious financial institution in the world has now run a tokenization pilot. JPMorgan, BlackRock, Citi, the Singapore monetary authority, every major bank in Switzerland. The asset-being-tokenized half of the equation is no longer interesting in itself. It's a checkbox.

The platforms whose pitch was "we tokenize X" are now competing on price, distribution, and which institution signed which custody agreement. None of those are durable.

What wallet-native means

Wallet-native is what comes next. It is not a synonym for tokenized. The two overlap, but the difference is the part that matters.

A tokenized asset, in the first-wave sense, can be held in many places. It is often custodied with the issuer, or with a regulated custodian, or in a dedicated wrapper account. The user can move it, but only inside a defined corridor. The asset is on-chain, but the asset is also still inside the issuer's pool.

A wallet-native asset lives in a wallet that the user controls, that the issuer cannot freeze without invoking a documented procedure, that any other protocol can integrate with without negotiating a side agreement, that can be combined with other wallet-native assets in the user's portfolio, that can move into a yield strategy, a lending protocol, a payment, or a hedge without leaving the surface it was issued on.

The distinction is custody and composability. A tokenized asset can be on-chain and still be effectively custodied by the issuer. A wallet-native asset is custodied by the user, and the rest of DeFi can build on top of it.

Why the second wave is harder

The reason the first wave got built first is that it is the easier of the two. Tokenizing an asset is largely a financial engineering exercise. You set up a custody arrangement, you wrap the asset, you issue a token, you publish the docs. The hard parts are real but they are mostly legal and operational. The architecture is conservative.

Wallet-native is harder because the architecture has to actively defend the property of the asset being held by the user. It has to handle redemption without the issuer having a kill-switch. It has to handle eligibility without a user-layer identity gate. It has to handle reconciliation across many possible holders, not just inside a closed pool. It has to support smart-contract wallets, programmatic integrations, and the long tail of weird things that DeFi-native users do with assets.

Each of those is a design problem, not a paperwork problem. The teams that ship the first-wave version are not necessarily the teams that ship the second-wave version, because the second wave requires a different mental model.

Why the demand is shifting

The reason I think the second wave is happening now, rather than in five more years, is that the user the first wave was built for is not the user who's actually showing up.

The first wave assumed the user was an institution with a regulated counterparty, doing one trade at a time, settling on a defined schedule. That user exists. They are slowly adopting tokenized infrastructure. They are also not where the volume is showing up.

The volume is showing up from users who already operate inside a wallet, who already hold stablecoins, who already use DeFi, and who want the rest of their portfolio to be inside the same surface. They do not want a tokenized asset that requires them to onboard at a custodian. They want an asset that lives in the wallet they already have.

Once that user has shown up in volume, the platforms whose architecture cannot serve them have to either rebuild or watch the volume go to platforms that can. That is the moment the second wave starts being a category instead of a thesis.

What this means for who wins

I think the platforms that win the second wave are not the same platforms that won the first. The first-wave winners built around regulated custody, institutional sales motions, and conservative legal structures. Those are real assets, but they are not the assets that produce a wallet-native architecture.

The second-wave winners are going to be the platforms that started from the wallet and worked outward to the asset. They are going to look more like protocol projects than like tokenization platforms. They are going to have a different shape of compliance, where the user-layer is permissionless and the asset-layer is gated. They are going to integrate with the rest of DeFi as a primary motion, not as an afterthought.

I am betting that GM Markets is one of those second-wave platforms. I might be wrong. There are a couple of teams who have been operating quietly that I think have a real shot at the same position. The market is wide enough for more than one of us to win, in the way that the stablecoin market has been wide enough for several issuers to coexist.

What I'm less sure about

The thing I keep turning over is the timing. I think the second wave is happening now, but I am not sure how long the transition takes. There is a version of this where the first-wave platforms manage to retrofit wallet-native architecture onto their existing systems and the transition happens inside the same set of names. There is another version where they cannot retrofit it without dismantling the business model that funds them, and a new set of names captures the second wave entirely. I do not know which version is right.

The honest answer is that the transition is probably going to be uneven. Some asset classes flip to wallet-native first, others lag. Some jurisdictions get there before others. Some user populations adopt the wallet-native version aggressively, others stay with the first-wave version because it is the path their compliance and operations teams already understand.

If I had to summarize what I think the next two years look like, it is that the word "tokenized" stops doing useful work in pitches, and the question shifts to whether the asset is actually wallet-native. The platforms that can answer yes get a shot at the second-wave demand. The platforms that cannot answer yes find that their first-wave moat compresses faster than they expected.

I might be too optimistic about the timing. I might be too pessimistic about the first-wave platforms' ability to adapt. The shape of the transition is going to be the next big argument in this space, and the founder on the panel who said "tokenized is going to stop being a feature" was, I think, naming the thing earlier than most of the room realized. Worth saying it again here so the framing is on the record.